XPO Logistics Announces Third Quarter 2021 Results

Reports highest revenue of any quarter in company history

Updates full year 2021 guidance based on higher-than-expected growth

Announces LTL network expansion of terminal capacity, trailer fleet and driver training in 2022

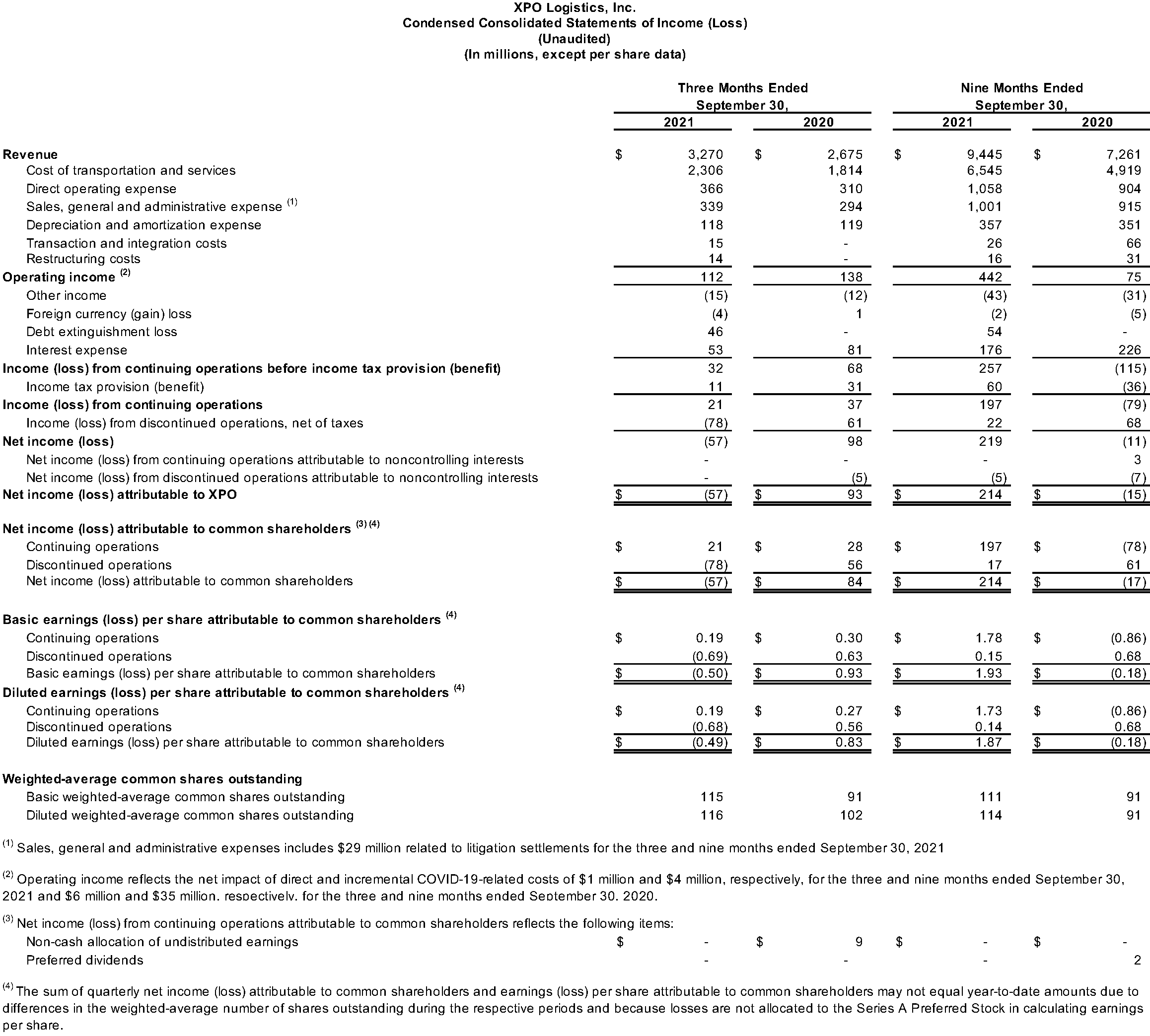

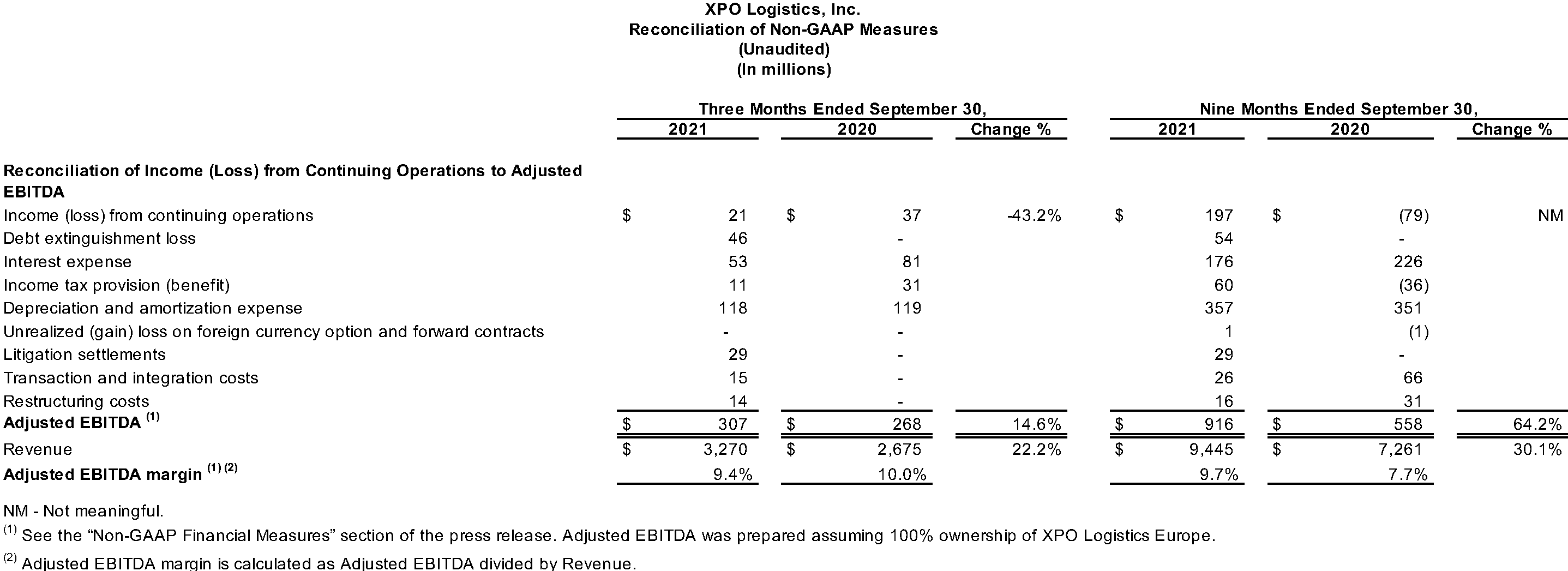

XPO Logistics, Inc. (NYSE: XPO) today announced its financial results for the third quarter 2021. Revenue increased to $3.27 billion for the third quarter, compared with $2.68 billion for the same period in 2020. Net income from continuing operations attributable to common shareholders was $21 million for the third quarter, compared with $28 million for the same period in 2020. Operating income was $112 million for the third quarter, compared with $138 million for the same period in 2020. Income from continuing operations was $21 million, compared with $37 million in prior year quarter. Diluted earnings from continuing operations per share was $0.19 for the third quarter, compared with $0.27 for the same period in 2020.

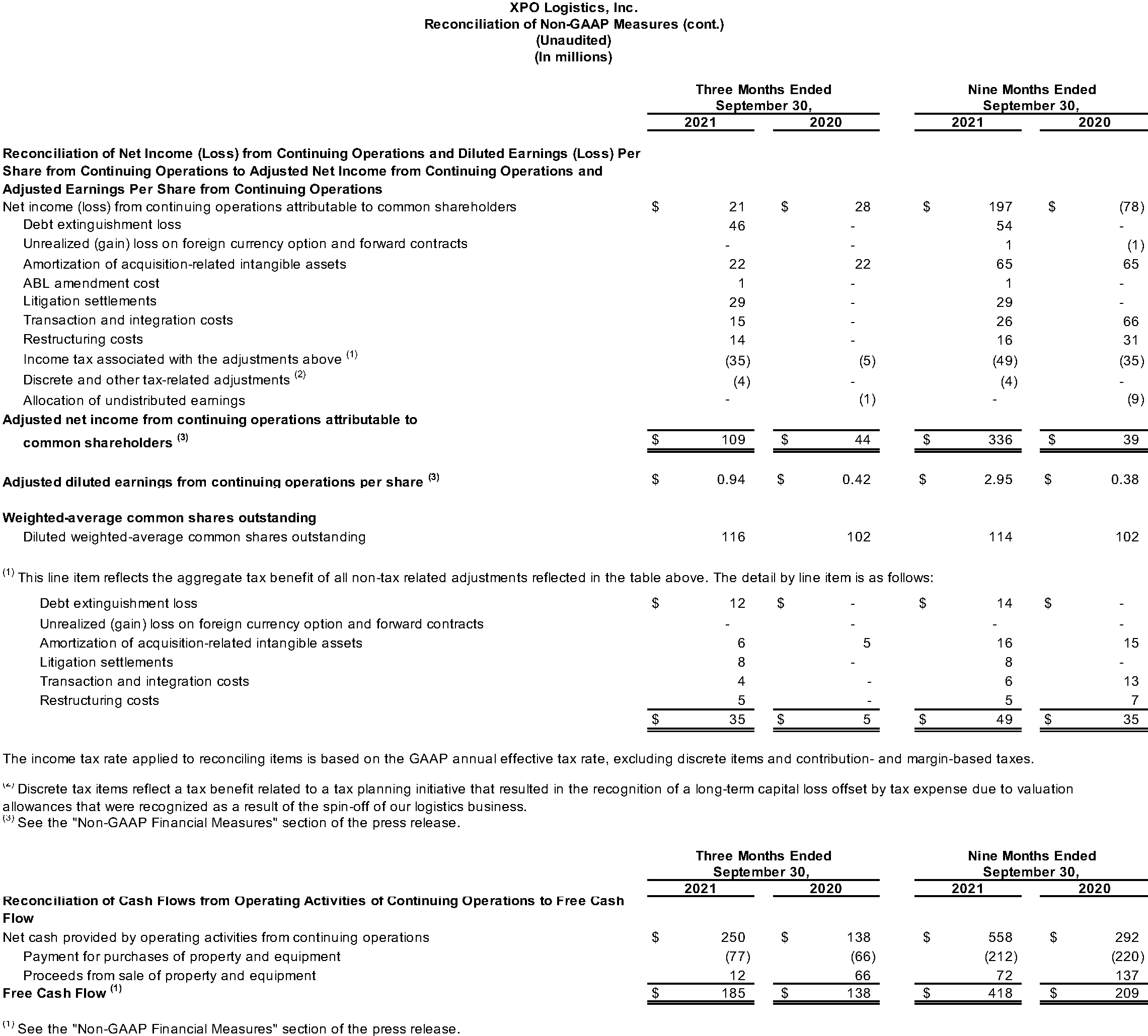

Adjusted net income from continuing operations attributable to common shareholders, a non-GAAP financial measure, was $109 million for the third quarter, compared with $44 million for the same period in 2020. Adjusted diluted earnings from continuing operations per share, a non-GAAP financial measure, was $0.94 for the third quarter, compared with $0.42 for the same period in 2020.

Adjusted earnings before interest, taxes, depreciation and amortization (“adjusted EBITDA”), a non-GAAP financial measure, increased to $307 million for the third quarter, compared with $268 million for the same period in 2020.

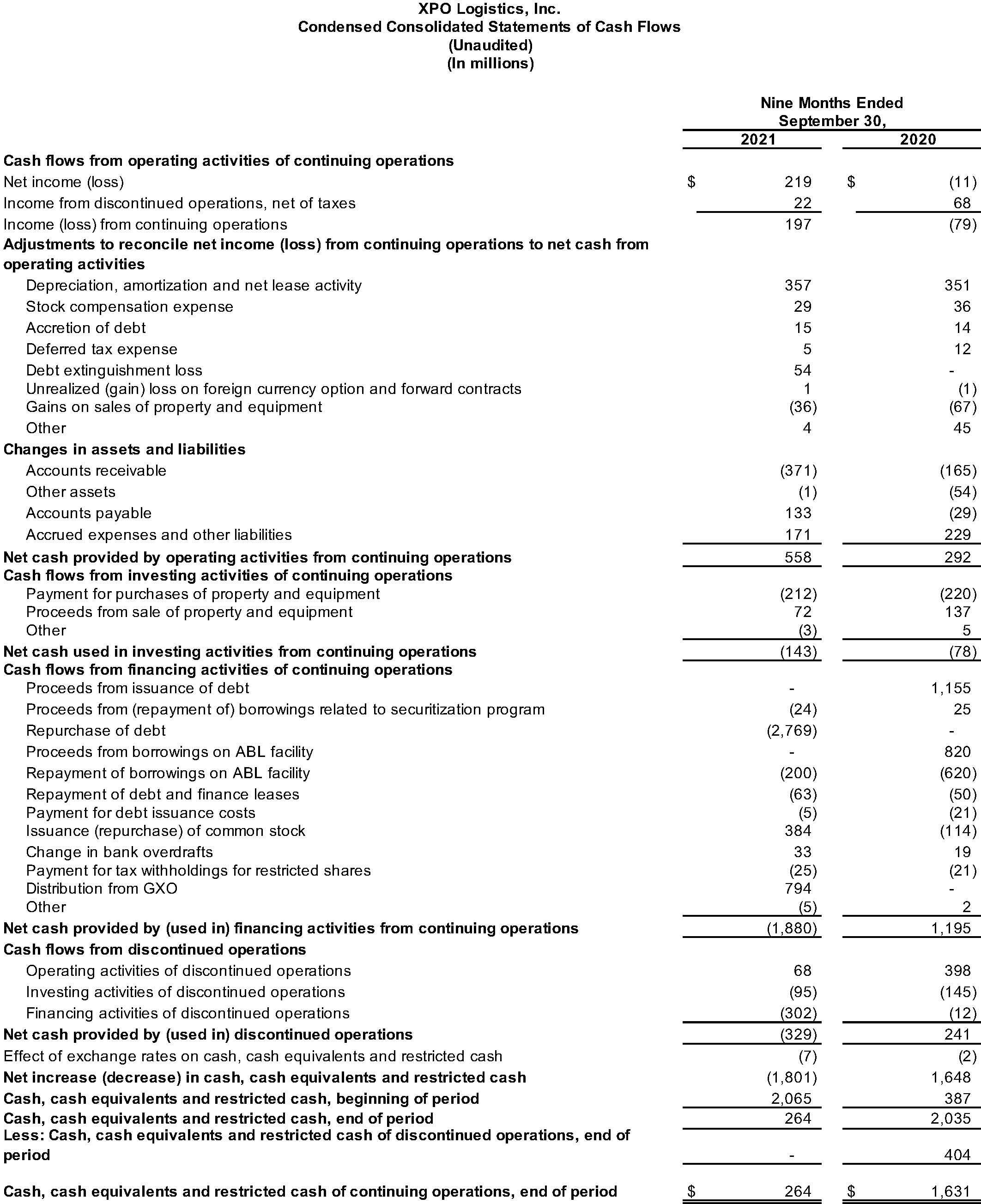

For the third quarter 2021, the company generated $250 million of cash flow from operating activities of continuing operations and $185 million of free cash flow, a non-GAAP financial measure.

Reconciliations of non-GAAP financial measures used in this release are provided in the attached financial tables.

2021 Updated Guidance

On November 2, 2021, the company updated its full year 2021 financial targets1, including a raise in fourth quarter adjusted EBITDA:

- Adjusted EBITDA of $300 million to $305 million generated in the fourth quarter, implying $1.228 billion to $1.233 billion of adjusted EBITDA for the full year, which increases the midpoint of the updated full year guidance to $1.231 billion — $16 million higher than the prior midpoint;

- Depreciation and amortization of $390 million to $395 million, excluding approximately $95 million of acquisition-related amortization expense, from a prior target of $385 million to $395 million;

- Interest expense2 of approximately $200 million, unchanged;

- Effective tax rate of 24% to 26%, from a prior target of 23% to 25%;

- Adjusted diluted EPS3 of $4.15 to $4.25, from a prior target of $4.00 to $4.30;

- Net capital expenditures of $250 million to $275 million, unchanged; and

- Free cash flow of $425 million to $475 million, from a prior target of $400 million to $450 million.

1The company’s full year 2021 pro forma financial targets have been calculated as if the August 2021 spin-off of the logistics segment had been completed on January 1, 2021. Guidance assumes 116 million diluted shares outstanding at year-end, and assumes current macroeconomic trends continue and labor and equipment shortages don’t worsen.

2Interest expense is presented on a pro forma basis; 2021 reported interest expense is expected to be approximately $230 million.

3Adjusted diluted EPS, assuming reported interest expense of approximately $230 million, would be a range of $4.00 to $4.05.

CEO Comments

Brad Jacobs, chairman and chief executive officer of XPO Logistics, said, “Company-wide we had an excellent third quarter, with record revenue and a solid beat on the bottom line. Our truck brokerage business had another phenomenal quarter, while our less-than-truckload results were mixed.

“In North American truck brokerage, every major metric was up year-over-year by large double-digits. We grew third quarter gross and net revenue in truck brokerage by 62%, on a 37% increase in load count per day. Our top 20 customers increased their total volume with us by 45%, and our share of wallet is trending up with key customers. These gains are being driven by our massive brokered capacity, robust digital capabilities and customer trust in our experienced brokerage leaders. We’ve tripled the number of customers on our XPO Connect digital platform from a year ago, and carrier usage is up over 100%. More than 550,000 drivers have downloaded the app to date.

“In North American LTL, we had our strongest yield growth yet, up 6% excluding fuel year-over-year. However, our operating ratio was negatively impacted by our decision to continue insourcing purchased transportation in the midst of driver and equipment constraints. We took actions that are gaining rapid traction — our yield growth accelerated again in October, and our network is more balanced now than it was a few weeks ago. We’re still targeting at least $1 billion of adjusted EBITDA in LTL in 2022. And over the next 12 to 24 months, we plan to invest more capital to expand our North American LTL door count by approximately 6% in key metros, following the 264-door Chicago Heights terminal we just opened.”

Jacobs concluded, “We raised our 2021 guidance for full year adjusted EBITDA to $1.228 billion to $1.233 billion, including a fourth quarter adjusted EBITDA increase to $300 million to $305 million. This reflects our third quarter results and our confidence in delivering a strong finish to the year across our business.”

North American LTL Strategic Actions

XPO is executing a company-specific action plan to enhance network efficiencies and drive growth in its high-ROIC LTL business, including:

- Improving network flow with selective freight embargoes, with the cost embedded in 2021 guidance;

- Driving pricing by pulling the January 2022 General Rate Increase forward to November, and instituting accessorial charges for detained trailers, oversized freight and special handling;

- Expanding the 2022 graduate count at XPO’s US driver training schools to more than double the nearly 800 graduates the company will have in 2021;

- Significantly increasing production capacity at XPO’s trailer manufacturing facility in Arkansas, with the expectation of nearly doubling the year-over-year number of units produced in 2022; and

- Importantly, allocating capital to expand North American LTL door count by 900 doors, or approximately 6%, over the next 12 to 24 months to improve network-wide operating efficiency and support future revenue growth.

Third Quarter 2021 Results by Segment

Starting with the third quarter of 2021, the company has two reporting segments, reflecting the spin-off of its logistics segment: North American Less-than-Truckload, and Brokerage and Other Services.

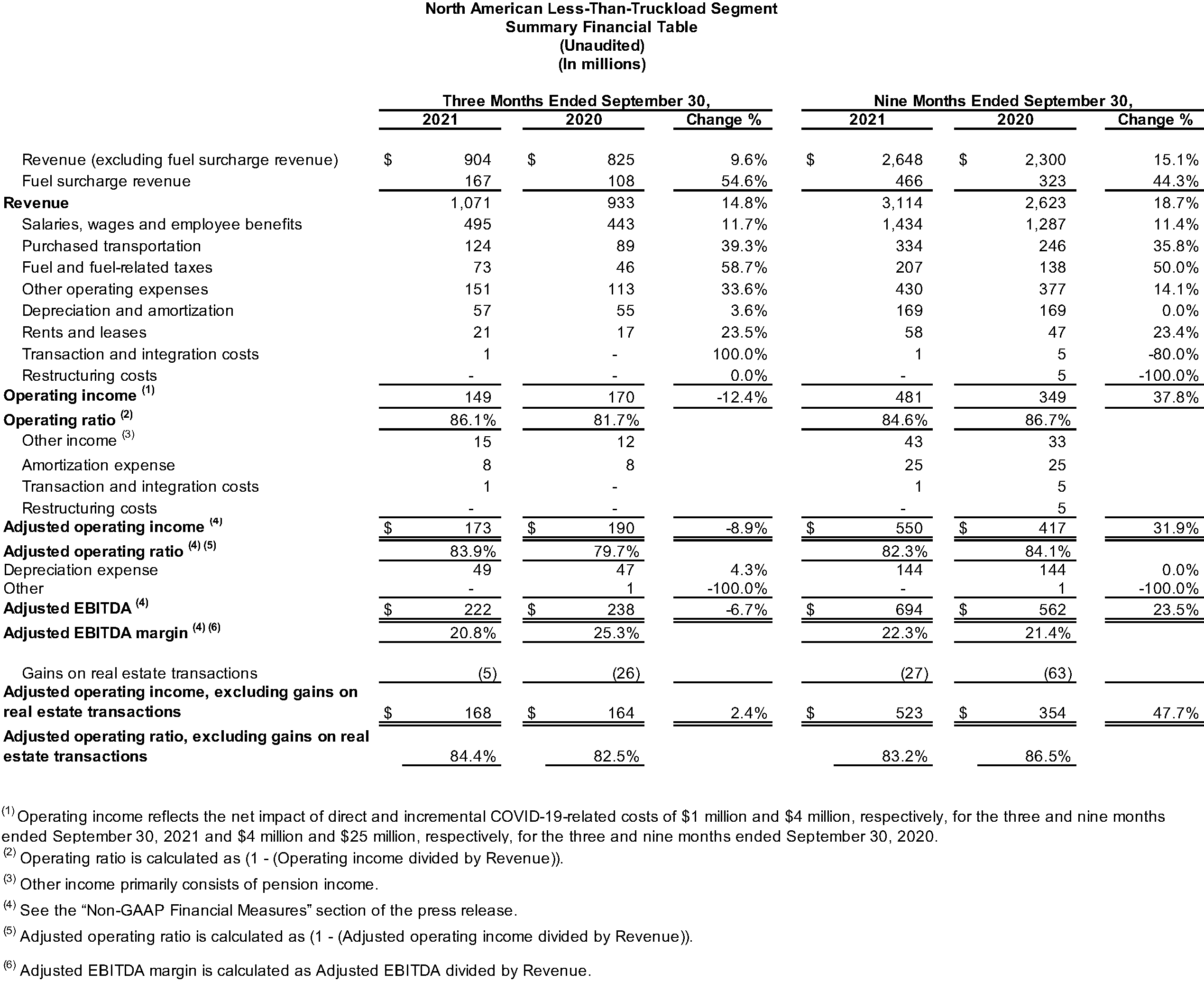

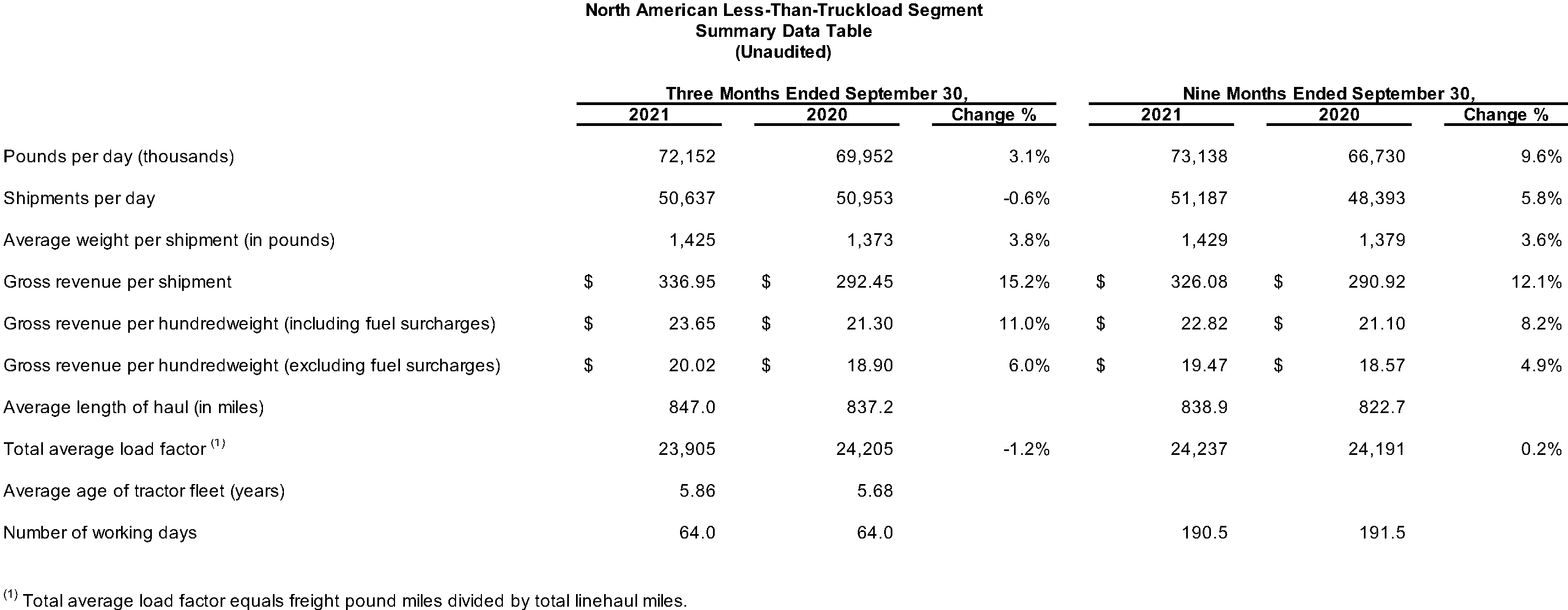

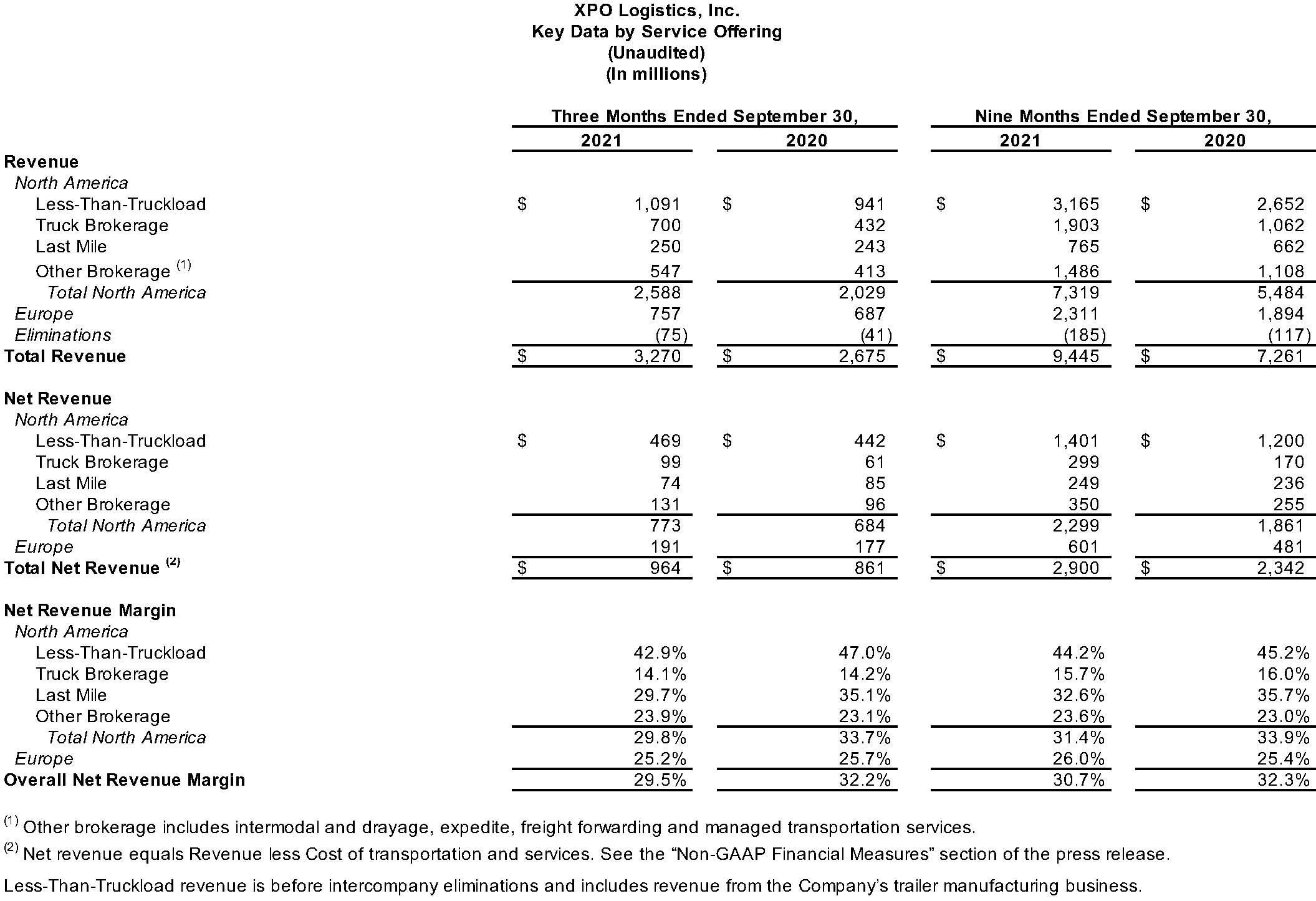

- North American Less-Than-Truckload: The segment generated revenue of $1.07 billion for the third quarter 2021, compared with $933 million for the same period in 2020. The year-over-year increase in segment revenue reflects an increase in average weight per day and yield.

Operating income for the segment was $149 million for the third quarter 2021, compared with $170 million for the same period in 2020. Adjusted EBITDA for the third quarter 2021 was $222 million, compared with $238 million for the same period in 2020. Adjusted EBITDA reflects a $5 million gain on sale of real estate in the third quarter of 2021, which is significantly lower than the $26 million gain for the same period in 2020. Adjusted EBITDA in the third quarter of 2021 also reflects higher revenue and lower COVID-19-related expenses, partially offset by increased compensation costs and purchased transportation expense incurred to meet growing demand.

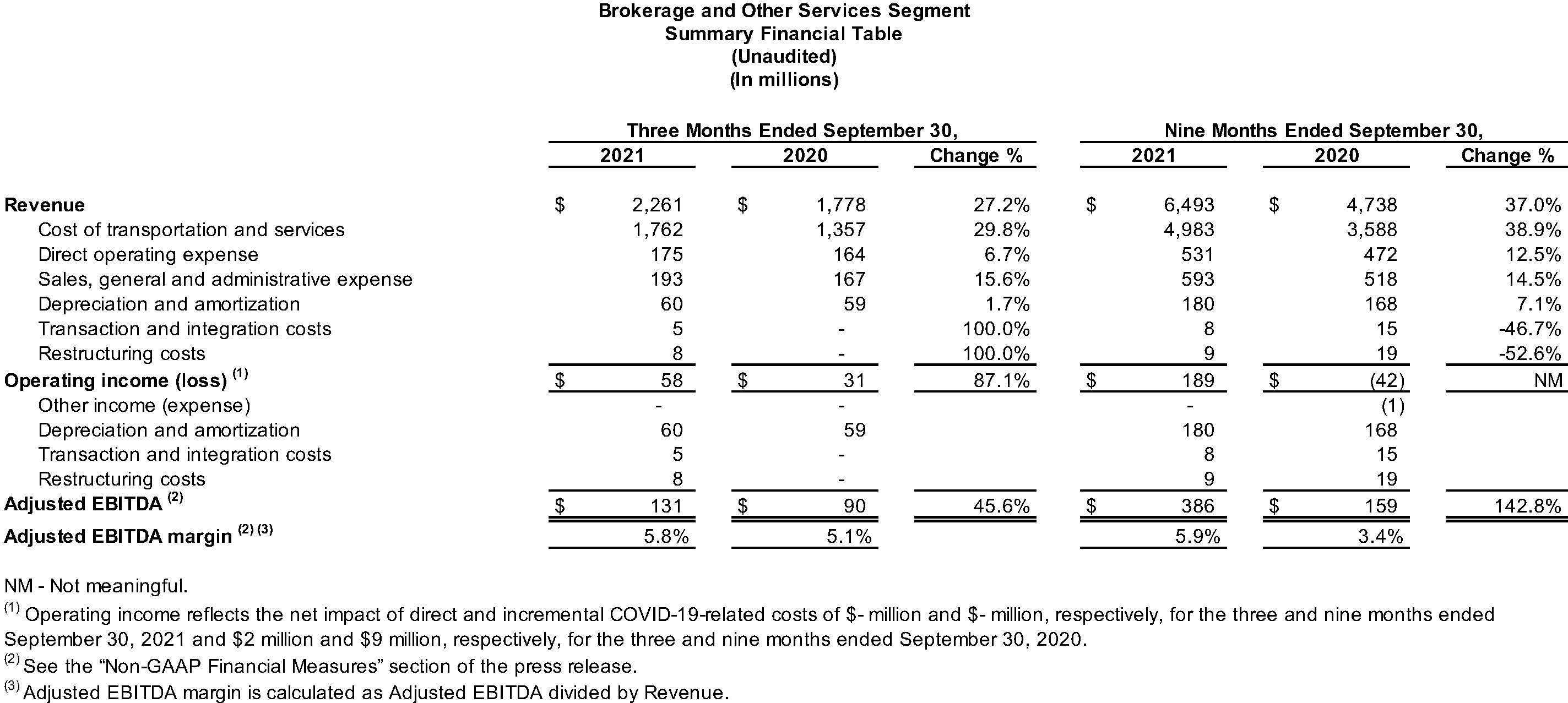

The third quarter operating ratio for the segment was 86.1% and the adjusted operating ratio was 83.9%. Excluding gains from sales of real estate, the LTL adjusted operating ratio was 84.4%. - Brokerage and Other Services: The segment generated revenue of $2.26 billion for the third quarter 2021, compared with $1.78 billion for the same period in 2020. The year-over-year increase in segment revenue reflects an increase in truck brokerage loads per day in North America and improved pricing across segment services, enhanced by the company’s digital platform, as well as improving market conditions in the recovery. These gains were partially offset by the impact of the global semiconductor shortage, which constrained customer demand for freight transportation services in North America and Europe, and by a truck driver shortage in the UK and North America.

Operating income for the segment was $58 million for the third quarter, compared with $31 million for the same period in 2020. Adjusted EBITDA was $131 million for the third quarter 2021, compared with $90 million for the same period in 2020. The year-over-year increase in adjusted EBITDA was primarily driven by higher revenue due to load growth and improved pricing, partially offset by higher compensation and facilities costs.

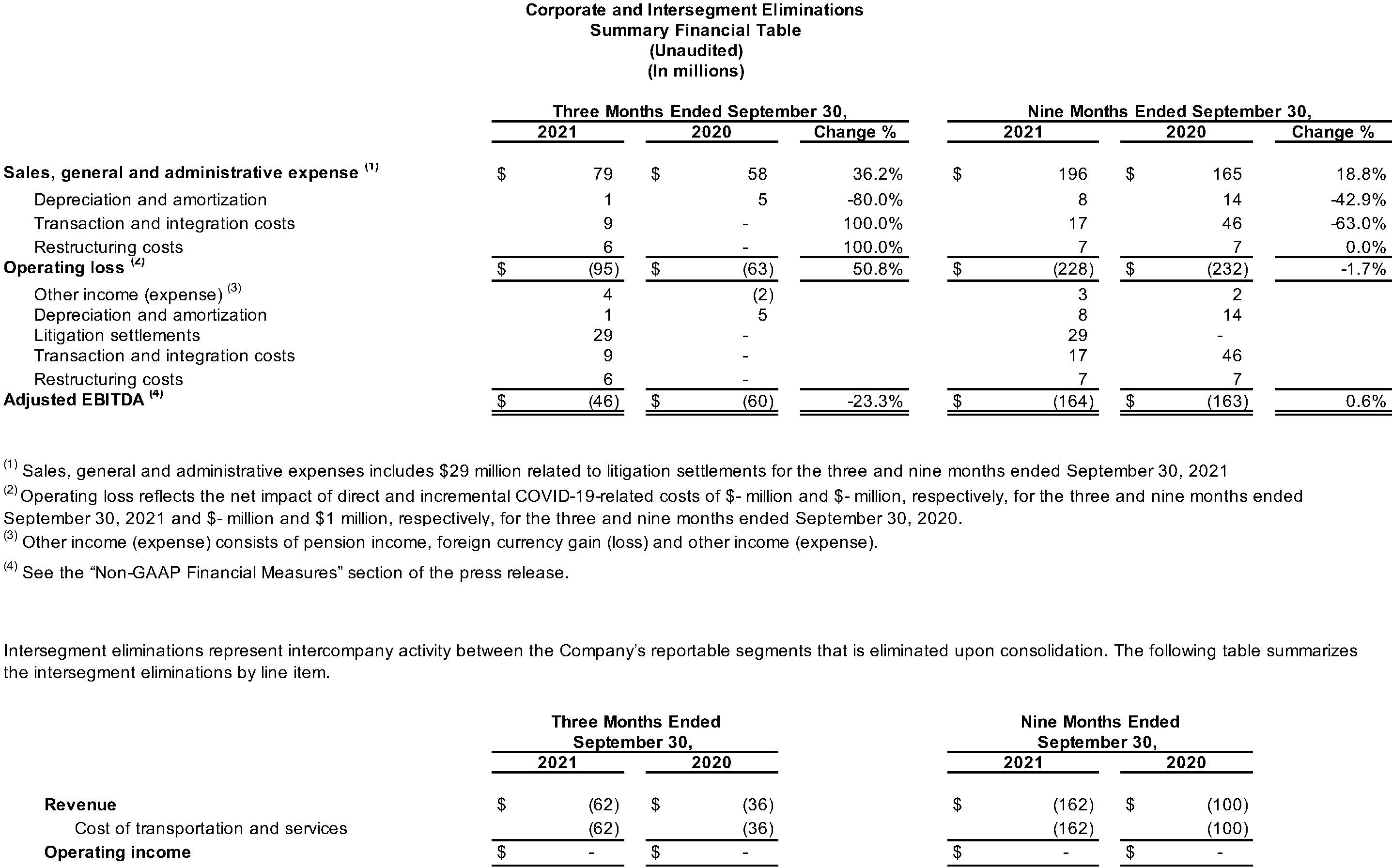

The company continued to significantly outperform the truck brokerage market in North America. Truck brokerage revenue in North America increased 62% year-over-year to $700 million for the third quarter, compared with $432 million for the same period in 2020. Net revenue increased 62% year-over-year to $99 million for the quarter, compared with $61 million for the same period in 2020. - Corporate: Corporate expense was $95 million for the third quarter of 2021, compared with $63 million for the same period in 2020. The year-over-year increase in corporate expense primarily reflects a legal settlement of $29 million and other discrete items in the third quarter of 2021. Corporate adjusted EBITDA, which excludes the discrete items, was an expense of $46 million for the third quarter of 2021, compared with an expense of $60 million for the same period in 2020, primarily reflecting lower insurance expense and third-party professional fees in the 2021 period.

Liquidity Position

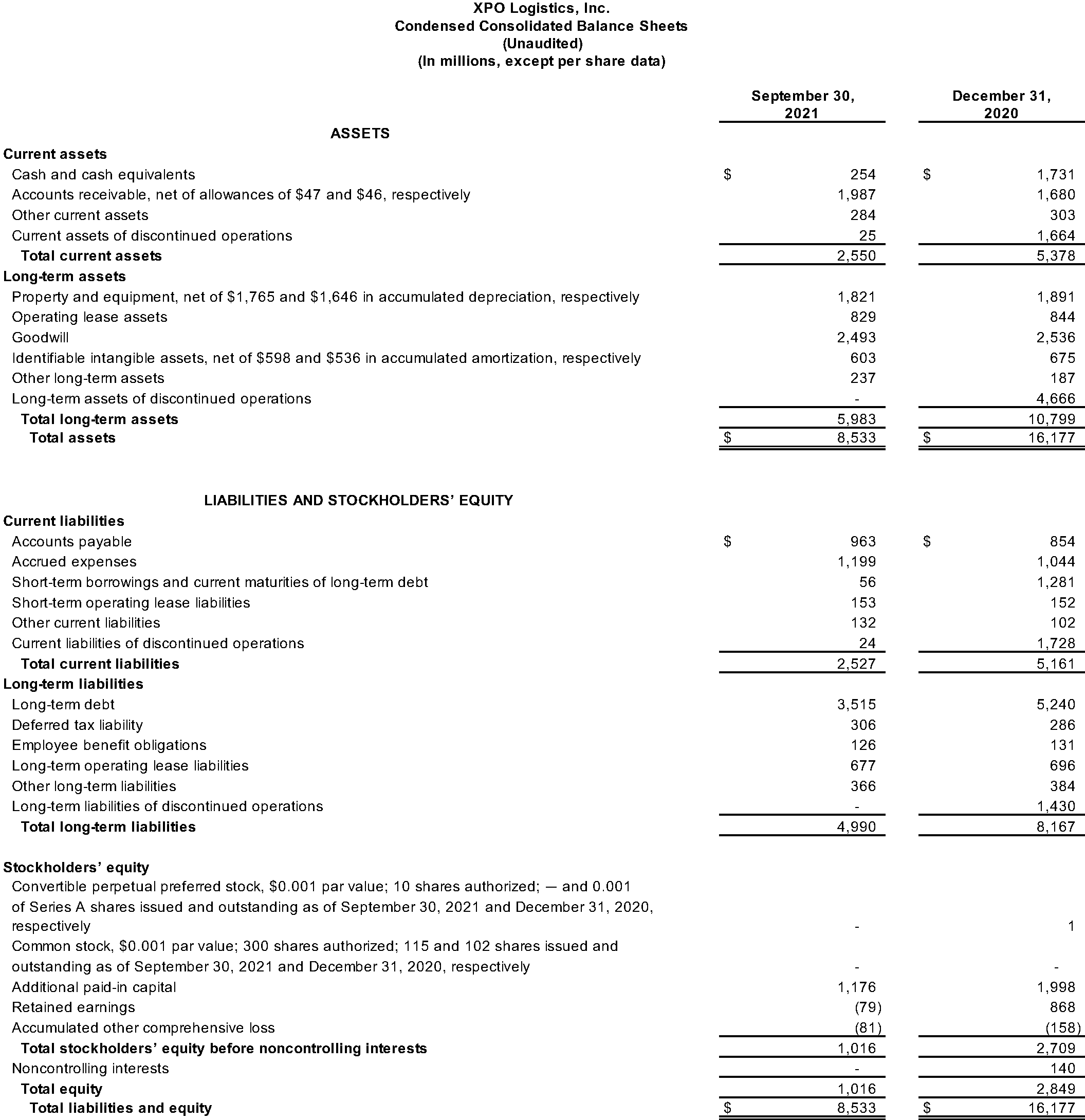

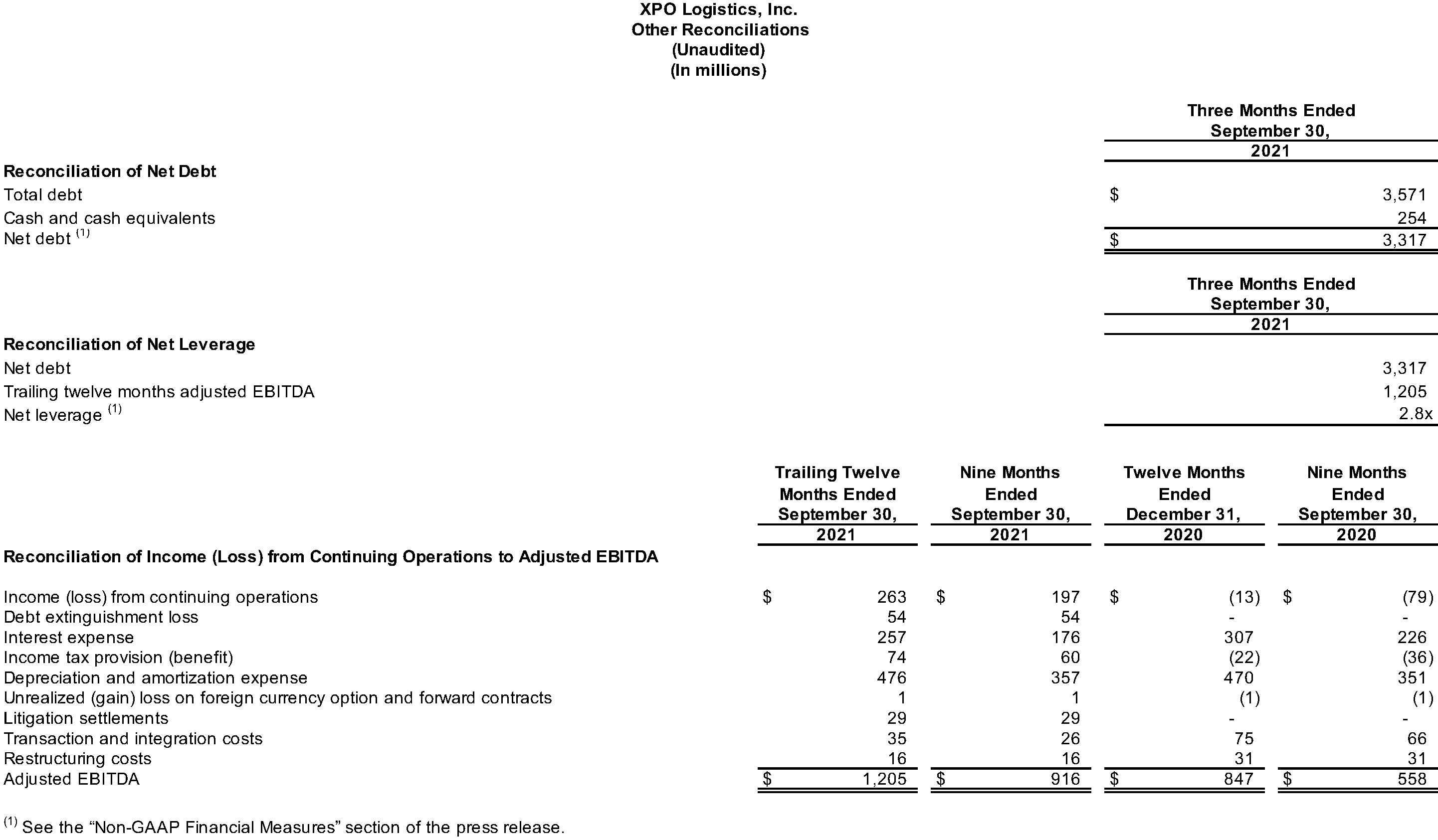

As of September 30, 2021, the company had over $1.2 billion of total liquidity, including $254 million of cash and cash equivalents and approximately $993 million of available borrowing capacity. The company’s net leverage was 2.8x, calculated as net debt of $3.3 billion, divided by adjusted EBITDA of $1.2 billion for the 12 months ended September 30, 2021.

Conference Call

The company will hold a conference call on Wednesday, November 3, 2021, at 8:30 a.m. Eastern Time. Participants can call toll-free (from US/Canada) 1-877-269-7756; international callers dial +1-201-689-7817. A live webcast of the conference will be available on the investor relations area of the company’s website, xpo.com/investors. The conference will be archived until December 3, 2021. To access the replay by phone, call toll-free (from US/Canada) 1-877-660-6853; international callers dial +1-201-612-7415. Use participant passcode 13724084.

About XPO Logistics

XPO Logistics, Inc. (NYSE: XPO) is a leading provider of freight transportation services, primarily truck brokerage and less-than-truckload (LTL). XPO uses its proprietary technology, including the cutting-edge XPO Connect® automated freight marketplace, to move goods efficiently through supply chains. The company’s global network serves 50,000 shippers with 756 locations and approximately 42,000 employees, and is headquartered in Greenwich, Conn., USA. Visit xpo.com and europe.xpo.com for more information, and connect with XPO on Facebook, Twitter, LinkedIn, Instagram and YouTube.

Non-GAAP Financial Measures

As required by the rules of the Securities and Exchange Commission (“SEC”), we provide reconciliations of the non-GAAP financial measures contained in this press release to the most directly comparable measure under GAAP, which are set forth in the financial tables attached to this release.

XPO’s non-GAAP financial measures for the three and nine months ended September 30, 2021 and 2020 used in this release include: adjusted earnings before interest, taxes, depreciation and amortization (“adjusted EBITDA”) and adjusted EBITDA margin on a consolidated basis and for our North American less-than-truckload and brokerage and other services segments as well as adjusted EBITDA for Corporate and Intersegment Eliminations; adjusted net income from continuing operations attributable to common shareholders and adjusted diluted earnings from continuing operations per share (“adjusted EPS”); net revenue and net revenue margin by service offering; free cash flows; adjusted operating income (including and excluding gains on real estate transactions) for our North American less-than-truckload segment; and adjusted operating ratio (including and excluding gains on real estate transactions) for our North American less-than-truckload segment. Also, XPO’s non-GAAP financial measures for the trailing twelve months ended September 30, 2021 and twelve months ended December 31, 2020 include adjusted EBITDA and for the three months ended September 30, 2021 include net leverage and net debt.

We believe that the above adjusted financial measures facilitate analysis of our ongoing business operations because they exclude items that may not be reflective of, or are unrelated to, XPO and its business segments’ core operating performance, and may assist investors with comparisons to prior periods and assessing trends in our underlying businesses. Other companies may calculate these non-GAAP financial measures differently, and therefore our measures may not be comparable to similarly titled measures of other companies. These non-GAAP financial measures should only be used as supplemental measures of our operating performance.

Adjusted EBITDA, adjusted net income from continuing operations attributable to common shareholders and adjusted EPS include adjustments for transaction and integration costs, as well as restructuring costs, litigation settlements and other adjustments as set forth in the attached tables. Transaction and integration adjustments are generally incremental costs that result from an actual or planned acquisition, divestiture or spin-off and may include transaction costs, consulting fees, retention awards, and internal salaries and wages (to the extent the individuals are assigned full-time to integration and transformation activities) and certain costs related to integrating and converging IT systems. Restructuring costs primarily relate to severance costs associated with business optimization initiatives. Management uses these non-GAAP financial measures in making financial, operating and planning decisions and evaluating XPO’s and each business segment’s ongoing performance.

We believe that free cash flow is an important measure of our ability to repay maturing debt or fund other uses of capital that we believe will enhance stockholder value. We calculate free cash flow as net cash provided by operating activities from continuing operations, less payment for purchases of property and equipment plus proceeds from sale of property and equipment. We believe that adjusted EBITDA and adjusted EBITDA margin improve comparability from period to period by removing the impact of our capital structure (interest and financing expenses), asset base (depreciation and amortization), litigation settlements, tax impacts and other adjustments as set out in the attached tables that management has determined are not reflective of core operating activities and thereby assist investors with assessing trends in our underlying businesses. We believe that adjusted net income from continuing operations attributable to common shareholders and adjusted EPS improve the comparability of our operating results from period to period by removing the impact of certain costs and gains that management has determined are not reflective of our core operating activities, including amortization of acquisition-related intangible assets, litigation settlements and other adjustments as set out in the attached tables. We believe that net revenue and net revenue margin improve the comparability of our operating results from period to period by removing the cost of transportation and services, in particular the cost of fuel, incurred in the reporting period as set out in the attached tables. We believe that adjusted operating income and adjusted operating ratio improve the comparability of our operating results from period to period by (i) removing the impact of certain transaction and integration costs and restructuring costs, as well as amortization expenses and (ii) including the impact of pension income incurred in the reporting period as set out in the attached tables. We believe that net leverage and net debt are important measures of our overall liquidity position and are calculated by removing cash and cash equivalents from our reported total debt and reporting net debt as a ratio of our last twelve-month reported adjusted EBITDA.

With respect to our financial targets for full year pro forma 2021 adjusted EBITDA, adjusted diluted EPS and free cash flow, and fourth quarter 2021 adjusted EBITDA, a reconciliation of these non-GAAP measures to the corresponding GAAP measures is not available without unreasonable effort due to the variability and complexity of the reconciling items described above that we exclude from these non-GAAP target measures. The variability of these items may have a significant impact on our future GAAP financial results and, as a result, we are unable to prepare the forward-looking statement of income and statement of cash flows prepared in accordance with GAAP that would be required to produce such a reconciliation.

Forward-looking Statements

This release includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, including our full year pro forma 2021 financial targets for adjusted EBITDA, depreciation and amortization (excluding acquisition-related amortization expense), interest expense, effective tax rate, adjusted diluted EPS, net capital expenditures and free cash flow; our fourth quarter 2021 financial target of adjusted EBITDA; and our 2022 financial target of at least $1 billion of adjusted EBITDA in the North American LTL segment. All statements other than statements of historical fact are, or may be deemed to be, forward-looking statements. In some cases, forward-looking statements can be identified by the use of forward-looking terms such as “anticipate,” “estimate,” “believe,” “continue,” “could,” “intend,” “may,” “plan,” “potential,” “predict,” “should,” “will,” “expect,” “objective,” “projection,” “forecast,” “goal,” “guidance,” “outlook,” “effort,” “target,” “trajectory” or the negative of these terms or other comparable terms. However, the absence of these words does not mean that the statements are not forward-looking. These forward-looking statements are based on certain assumptions and analyses made by us in light of our experience and our perception of historical trends, current conditions and expected future developments, as well as other factors we believe are appropriate in the circumstances.

These forward-looking statements are subject to known and unknown risks, uncertainties and assumptions that may cause actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by such forward-looking statements. Factors that might cause or contribute to a material difference include the risks discussed in our filings with the SEC and the following: economic conditions generally; the severity, magnitude, duration and aftereffects of the COVID-19 pandemic, including supply chain disruptions due to plant and port shutdowns and transportation delays, the global shortage of certain components such as semiconductor chips, strains on production or extraction of raw materials, cost inflation and labor and equipment shortages, which may lower levels of service, including the timeliness, productivity and quality of service, and government responses to these factors; our ability to align our investments in capital assets, including equipment, service centers and warehouses, to our customers’ demands; our ability to implement our cost and revenue initiatives; our ability to successfully integrate and realize anticipated synergies, cost savings and profit improvement opportunities with respect to acquired companies; matters related to our intellectual property rights; fluctuations in currency exchange rates; fuel price and fuel surcharge changes; natural disasters, terrorist attacks or similar incidents; risks and uncertainties regarding the expected benefits of the spin-off of our logistics segment; the impact of the spin-off on the size and business diversity of our company; the ability of the spin-off to qualify for tax-free treatment for U.S. federal income tax purposes; our ability to develop and implement suitable information technology systems and prevent failures in or breaches of such systems; our substantial indebtedness; our ability to raise debt and equity capital; fluctuations in fixed and floating interest rates; our ability to maintain positive relationships with our network of third-party transportation providers; our ability to attract and retain qualified drivers; labor matters, including our ability to manage our subcontractors, and risks associated with labor disputes at our customers and efforts by labor organizations to organize our employees; litigation, including litigation related to alleged misclassification of independent contractors and securities class actions; risks associated with our self-insured claims; risks associated with defined benefit plans for our current and former employees; and governmental regulation, including trade compliance laws, as well as changes in international trade policies and tax regimes; governmental or political actions, including the United Kingdom’s exit from the European Union; and competition and pricing pressures.

All forward-looking statements set forth in this release are qualified by these cautionary statements and there can be no assurance that the actual results or developments anticipated by us will be realized or, even if substantially realized, that they will have the expected consequences to or effects on us or our business or operations. Forward-looking statements set forth in this release speak only as of the date hereof, and we do not undertake any obligation to update forward-looking statements to reflect subsequent events or circumstances, changes in expectations or the occurrence of unanticipated events, except to the extent required by law.